Resident Associate

Manager, Trade 'n Technology Program

Cover Image: A car hauler carries Toyota RAV4 vehicles as it enters to cross the Ambassador Bridge in Windsor, Ontario to go to Detroit, Michigan on February 3, 2025. (Photo by JEFF KOWALSKY/AFP via Getty Images)

The condition of America’s auto industry depends on where one looks. On paper, Detroit’s big three—General Motors, Ford, and Stellantis—remain profitable, anchored by a steady domestic market for SUVs and pickups. Yet beneath those earnings lies a brittle structure: shrinking competitiveness abroad, mounting production costs at home, and a conspicuous inability to deliver affordable vehicles at scale. The result is an industry that looks stable from a distance but, on closer inspection, is badly exposed.

Many in Washington point to China as the culprit. The “China shock” of the early 2000s is often blamed for hollowing out U.S. manufacturing. But in autos, that narrative is misleading. Detroit’s retreat from small cars and supplier networks long predated China’s WTO accession. The true competitive blows came from Japanese and European firms that had already built leaner, more efficient models. China’s later surge in EVs did not create America’s decline—it simply exploited the space left behind.

Meanwhile, the U.S. consumer market itself has become a structural liability. Demand and supply are badly out of sync. Americans are holding onto their cars longer than ever before: by 2025, the average age of vehicles on U.S. roads had reached 12.5 years, an all-time high. This is not because households love their old sedans, but because the market is failing to provide affordable new options. Supply bottlenecks and high sticker prices have slowed replacement, even as a rising share of the fleet approaches the end of its usable life.

That aging fleet makes the need for industrial transition urgent. The question is no longer whether U.S. consumers will shift, but how—and with what vehicles. At present, the most viable pathway is electrification. EVs, already scaling abroad, are the benchmark for whether the U.S. can rebuild capacity in time. Hybrids (HEVs) may also play a role, particularly in segments where full electrification is costlier or less practical. But whichever path dominates, one fact is clear: the U.S. auto industry cannot meet this transition with its current structure.

As the electrification transition looms and expands over the past decades, EV as a branch of auto development is no longer considered innovative. Amid the growing market of EVs, however, the U.S. companies’ failure in adapting and catching up on the trend is a testament of its deep inherent structural problem. EVs are not just another product cycle—they are the benchmark for whether an auto industry has the scale and depth to compete globally. Unlike infotainment gimmicks or marginally better engines, electrification requires an entire system to move: batteries, charging networks, raw materials, and consumer adoption. Europe, China, Japan, and Korea have all built strategies around that reality.

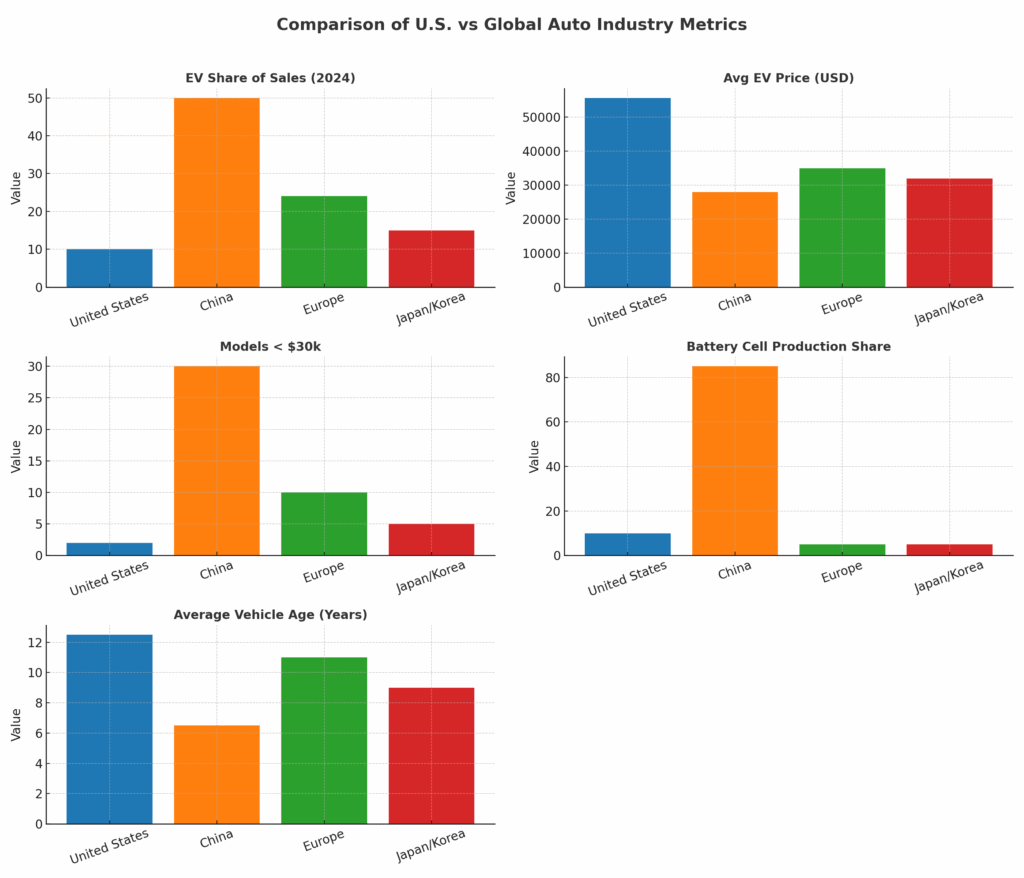

Europe hardwired EVs into its climate agenda: strict emissions caps, combustion bans in the 2030s, and subsidies for charging networks. Volkswagen and Renault retooled for compact and mid-market EVs. Now, nearly one in four new European cars is electric.

China treated EVs as an industrial strategy from the start. Since the mid-2000s, Beijing has pumped money into not just assembly, but lithium refining, cathode chemistry, and graphite processing. By 2024, half of all new cars sold in China—around 11 million—were electric. That scale brought costs down across the industry, allowing BYD and others to sell profitable EVs below $30,000.

Japan and Korea fused EVs into their long-standing efficiency culture. Toyota expanded from hybrids into multiple EV lines, while Hyundai and Kia became serious global players with affordable, high-quality EVs. Their advantage lies in decades of cost discipline and lean supply chains.

The United States? Stuck with SUVs and pickups. Detroit’s big three invested in EVs, but not fast enough and not at sufficient scale. American consumers are wedded to size, and cheap gasoline—$3.13 a gallon in 2025 versus $6–7 in Europe—meant there was little economic pressure to shift. Add in Corporate Average Fuel Economy (CAFE) standards that treat SUVs as “light trucks” with laxer requirements, and Detroit doubled down on high-margin big vehicles and hybrids while ceding the entry-level market, which, unsurprisingly, led to their full retreat from the EV development.

The result is structural vulnerability. Larger vehicles demand bigger batteries, which drive up costs. Without small, affordable EVs to scale production, U.S. automakers remain locked in a high-cost trap. What looked like a savvy domestic strategy is now a liability abroad. EVs are therefore the test case: fail here, and the U.S. auto sector risks becoming globally irrelevant—profitable only in its home market, but detached from where growth really is.

The struggles of today’s auto industry cannot be separated from the broader trajectory of U.S. manufacturing decline. Beginning in the late 1970s, the American economy pivoted decisively toward financialization and services. Capital increasingly flowed into short-term financial instruments—stock buybacks, leveraged mergers, and speculative markets—rather than long-horizon investments in plants, equipment, and workforce development. The ethos of shareholder primacy dictated that managers deliver quarterly returns, even at the cost of long-term competitiveness. For automakers, this translated into aggressive outsourcing of parts and components, thinning supplier networks, and a willingness to hollow out domestic capacity so long as margins could be preserved in the short run.

This structural shift collided with a series of external shocks. The oil crises of 1973 and 1979 were particularly devastating for Detroit. For decades, American manufacturers had built their brand identities around large sedans and muscle cars. Suddenly, consumers faced gasoline prices that made such vehicles impractical. Japanese and European automakers, which had long specialized in smaller, fuel-efficient cars, seized the opening. Imports from Toyota, Honda, and Volkswagen soared. By the mid-1980s, Japanese brands held more than 20 percent of the U.S. market, while General Motors’ domestic market share plunged from over 50 percent in the 1960s to under 35 percent.

U.S. policymakers did respond. The 1975 Energy Policy and Conservation Act introduced Corporate Average Fuel Economy (CAFE) standards, designed to push automakers toward more efficient vehicles. Yet the design of the regulations contained a crucial loophole: SUVs and light trucks were subject to less stringent requirements. Detroit leaned into this exception. Rather than investing heavily in small-car platforms, U.S. automakers shifted their portfolios toward pickups and SUVs—vehicles that were profitable domestically but misaligned with long-term global trends. This strategic choice stabilized earnings but entrenched a structural weakness: the loss of competitiveness in compact and mid-sized vehicles, precisely the segments where international competition was most intense.

Meanwhile, other advanced economies took divergent paths. Europe responded to the oil shocks by locking in efficiency through permanent high fuel taxes and later carbon-based regulations. Automakers like Volkswagen, Peugeot, and Fiat embedded fuel economy and compactness as baseline design imperatives. Japan doubled down on its keiretsu supplier system, ensuring tight coordination between assemblers and component makers. This ecosystem allowed Japanese firms to improve quality and cost discipline year after year, culminating in Toyota’s rise as the global benchmark for lean production. By the 1990s, Toyota and Honda were not only dominant in compact cars but had also begun competing in larger segments with vehicles like the Accord and Camry—models that combined efficiency with reliability and steadily eroded Detroit’s consumer base.

China’s story came later but followed the same logic of aligning national policy with industrial strategy. Starting in the 2000s, Beijing employed targeted incentives, phased fuel economy standards, and investment in domestic suppliers to build the foundations of a national auto industry. When the EV opportunity emerged, China leapfrogged the internal-combustion incumbency altogether. Without a legacy of oversized vehicles or entrenched labor contracts, Chinese firms could start fresh, scaling battery technology and compact EV models just as global demand shifted.

Today’s picture is the cumulative result of these decades-long divergences. The world’s growth segments—compact EVs, affordable hybrids, efficient mid-sized cars—are dominated by competitors of American automakers. The United States retains engineering excellence, yet its manufacturing ecosystem has become narrowly profitable at home and strategically irrelevant abroad. The crossroads is not new—it is the end point of a forty-year trajectory where policy choices, consumer culture, and financialized corporate strategies consistently favored short-term profitability over long-term capacity.

On the surface, U.S. EV demand still appears solid. In the fourth quarter of 2024, U.S. EV sales surged 15.2% year‑over‑year, setting a new quarterly record with 365,824 units sold, and full-year EV sales hit 1.3 million—a 7.3% increase from 2023. The upward trajectory continued into 2025: in Q1, nearly 300,000 EVs were sold, up 11% compared to the same period last year.

But beneath the headline growth lies a structural mismatch: demand is outpacing what Detroit can actually deliver. On the consumer side, surveys suggest that about 24% of vehicle shoppers say they are “very likely” to consider purchasing an EV, with another 35% “somewhat likely”. These figures underscore genuine interest, but sales data show the supply side—especially from legacy automakers—can’t meet it with affordable options.

Globally, EV adoption has already reached scale. In 2024, 17 million EVs were sold worldwide—over 20 percent of all cars sold. Nearly half of China’s new cars were electric, totaling 11 million; Europe reached almost one in four. The U.S. market share slipped to 9.6 percent in Q1 2025, down from 10.9 the quarter before. The decline was not due to lack of demand—overall sales volumes were higher—but because domestic production cannot deliver affordable vehicles at scale.

Price is the biggest barrier. The average EV in the U.S. cost over $55,000 in 2024, compared with $36,500 for compact SUVs—the segment that anchors American demand. The result is a bifurcated market: Tesla dominates the high end, selling EVs as premium goods, while affordable mass-market options are almost nonexistent. In fact, the IEA reports that only two models available in the U.S. retailed below $30,000. Chinese and European automakers, by contrast, already field dozens of such models.

Supply chain dependence compounds the issue. China controls 85 percent of global EV battery cell production and 90 percent of key materials processing. Even new U.S. gigafactories rely on imported cathodes, anodes, and processed graphite. As long as Detroit lacks control over these inputs, costs stay high.

This creates a perverse outcome: American EV demand is real and growing, but the supply comes either from Tesla—positioned increasingly as a luxury brand—or from foreign producers. Detroit’s legacy firms, still tethered to SUVs and pickups, simply cannot deliver competitive EVs. The result is not an absence of buyers, but an absence of affordable, domestically built cars to sell them.

The data, in other words, show a market being pulled in opposite directions: rising consumer demand colliding with stagnant domestic capacity. That tension explains why the U.S. has slipped below the global curve and why, unless production bottlenecks are addressed, America’s EV future will either be imported—or priced out of reach.

The defining feature of today’s U.S. auto industry is a structural “capacity trap.” It is not that American engineers cannot design EVs, nor that consumers lack interest. It is that the production ecosystem cannot scale in a way that drives down costs and feeds mass adoption. Without scale, costs remain high; with high costs, adoption stagnates; and without adoption, new capacity is never justified. This loop – from capacity building to cost reduction, from adoption increase to further capacity expansion—has become the central constraint on the industry.

A cycle of insufficient scale

Automakers understand that EV production must achieve scale quickly to compete globally. Yet U.S. factories remain stuck in a volume band that is too low to unlock efficiency. Assembly plants like GM’s soon to be closed Factory ZERO or Ford’s EV truck lines, which is finally going to release a midsize EV truck at $30,000 by 2027, are still at the initial stage of the capacity building loop, while Japanese, Korean, Chinese and European plants measure capacity in the hundreds of thousands. Economies of scale in EVs are brutal: unless production volumes exceed a certain threshold, fixed costs for tooling, gigafactory investment, and supplier development cannot be spread effectively. American firms are caught in the middle ground—too big to be artisanal, too small to be cost-competitive.

The battery bottleneck

The supply chain reinforces this trap. Batteries are the single largest cost component of an EV, and the United States does not yet control the mid-stream processing that makes batteries cheap. Even as gigafactories such as Ultium Cells and BlueOval SK come online, they remain dependent on imported cathodes, anodes, and processed graphite. These inputs are overwhelmingly supplied by China, which controls around 90 percent of global processing. This dependence means U.S. cell production will remain vulnerable to foreign pricing power. Even if domestic cell plants reduce logistics costs, the bulk of the bill of materials is still set abroad.

Market structure and product mix

The American consumer market compounds the problem. With 62 percent of new vehicle sales classified as trucks in 2023, electrification requires larger vehicles with much larger battery packs. A compact EV in China may require a 40 kWh pack; a U.S. pickup truck may demand over 100 kWh. The cost difference is not linear—larger packs drive up not just raw material demand but also thermal management, chassis design, and charging infrastructure. This means American automakers face a higher baseline cost curve simply because their domestic market favors heavier vehicles.

Pricing pressure and consumer adoption

The outcome is predictable: EVs in the U.S. remain priced far above what mainstream consumers will pay. Kelley Blue Book data show the average EV transaction price at $55,700, compared with $36,500 for compact SUVs. This $20,000 gap explains why EV adoption in the U.S. slipped to 9.6 percent in Q1 2025, even as global adoption surged past 20 percent. With subsidies now being rolled back, there is little to offset the price differential. Without higher adoption, new investments in scale remain financially risky, reinforcing the trap.

A closed loop

In effect, the U.S. industry is trapped in a feedback loop. Limited capacity ensures high costs; high costs depress adoption; low adoption discourages new investment in capacity. Competitors in China and Europe have already broken this loop through sustained policy support and scale-building strategies. America has not. And as long as the U.S. remains structurally tied to larger vehicles and foreign inputs, the capacity trap will persist.

This is not a problem of innovation. American engineers and startups can design cutting-edge EVs. It is a problem of industrial organization: the inability to produce cheaply and at scale. Until that loop is broken, the U.S. will remain a high-cost niche player in the global EV market—innovative on paper, but uncompetitive in practice.

If America’s auto industry is trapped by capacity constraints, then the obvious question is whether government policy can provide an escape. Washington has, in fact, tried two major approaches: tariffs and subsidies. Both have been deployed repeatedly over the last decade. Yet both have failed to generate the kind of sustainable, cost-competitive capacity needed to transform the industry. Instead, they have either raised prices or provided only temporary fiscal scaffolding that is now being dismantled.

Tariffs have long been the instinctive tool of U.S. trade policy, and EVs are no exception. In 2024, the administration imposed 100 percent tariffs on Chinese EVs, alongside new duties on batteries, cathodes, anodes, and processed graphite. These measures were meant to shield domestic producers from low-cost imports. In practice, they function more like a price escalator. American automakers still depend heavily on imported mid-stream materials—particularly processed graphite and cathode active materials—which China controls at scale. Tariffs on those inputs drive up the costs of domestic EV production instead of lowering them. They provide symbolic protection but no new factories, no supplier depth, and no economies of scale.

Moreover, tariffs cannot alter domestic consumer preference. Even if Chinese EVs are priced out of the U.S. market, American consumers are not suddenly given access to affordable domestic alternatives. Without local capacity to produce compact EVs at $25,000–$30,000, the tariff wall simply ensures that U.S. buyers face fewer choices at higher prices. Tariffs buy time, but time without parallel investment only entrenches the capacity trap further.

If tariffs raise prices, subsidies try to mask them. The Inflation Reduction Act (IRA) was the most ambitious attempt in recent memory to spur EV adoption and localize supply chains. Through tax credits for consumers, loans for gigafactories, and incentives for domestic sourcing, it sought to bridge the gap between high American costs and affordable global benchmarks. For a time, it worked: sales ticked upward in 2023 and early 2024, and several new battery plants broke ground.

Yet the IRA also revealed the limits of subsidies. Compliance rules were complex, eligibility requirements constantly shifting, and fiscal costs steep. Automakers complained about uncertainty in how credits would be applied, while consumers struggled to understand which vehicles qualified. Most importantly, subsidies did nothing to resolve the underlying supply chain asymmetry. American firms still depended on imported cathodes, anodes, and graphite. Subsidies could offset the pain but not build capacity.

Now, even that imperfect framework is vanishing. This year, the GOP-controlled Congress moved to terminate federal EV tax credits by September 30, with clean-energy incentives rolled back more broadly as part of fiscal retrenchment. The very scaffolding that kept American EVs marginally competitive is being dismantled. Automakers face the same structural cost disadvantages—only now without federal support to cushion the gap.

The result is a vacuum. Tariffs inflate costs without adding capacity. Subsidies that masked those costs are disappearing. No coherent industrial policy exists to target the real bottlenecks: mid-stream materials processing, small-car platforms, and scaled domestic assembly. Instead, Washington defaults to defensive measures that either raise consumer prices or distribute temporary fiscal band-aids.

This is not a uniquely American problem—Europe and Japan also face rising costs and supply-chain dependencies. But they have paired subsidies and tariffs with aggressive structural policies: high fuel taxes that lock in efficiency, industrial planning to build supplier ecosystems, and coordinated consumer incentives to boost adoption. The United States has done none of these at scale. Instead, its approach remains fragmented, short-lived, and politically unstable.

In short, tariffs and subsidies have proven inadequate not because they are misguided per se, but because they are deployed without a long-term industrial strategy. Tariffs buy time but do not build plants. Subsidies stimulate adoption but do not alter cost structures. And both are subject to political swings that undermine investor confidence. As long as this remains the case, existing policies cannot resolve the capacity trap—they can only disguise it, briefly and imperfectly, before the underlying constraints reassert themselves.

The weakness of America’s auto industry is not brains—it’s brawn. Detroit still has engineers, designers, and innovators. What it lacks is the muscle of scaled production. For decades, cheap gas, SUV profits, and regulatory loopholes allowed it to duck the reckoning. Now, with EVs reshaping the global market, the bill is due.

The world has already moved: EVs are past 20 percent of global sales. China sells nearly half its new cars as electric. Europe is closing in on one in four. The U.S. is stuck below 10 percent, with average prices $20,000 above what mainstream buyers will pay. Affordable models are absent, supply chains are foreign, and consumer preferences only raise costs further.

Tesla does not change this picture—it highlights it. Washington’s tariffs inflate prices; Biden’s IRA, once sold as industrial salvation, has already been scrapped. America is left with no strategy beyond improvisation.

Unless the U.S. builds real domestic capacity—cells, materials, and affordable models—it will remain a two-tier auto economy: strong only at home in trucks and SUVs, but increasingly irrelevant abroad where the future is being written. Innovation without production is an idea without a market. And Detroit, for now, is stuck in neutral.

The Institute for China-America Studies is an independent nonprofit, nonpartisan research organization dedicated to strengthening the understanding of U.S.-China relations through expert analysis and practical policy solutions.

1919 M St. NW Suite 310,

Washington, DC 20036

icas@chinaus-icas.org

(202) 968-0595

© 2026 INSTITUTE FOR CHINA-AMERICA STUDIES. ALL RIGHTS RESERVED.

Canada eases EV tariffs on China with quota system, opening new market access