ICAS Trade ‘n Tech Dispatch (online ISSN 2837-3863, print ISSN 2837-3855) is published about every two weeks throughout the year at 1919 M St NW, Suite 310, Washington, DC 20036.

The online version of ICAS Trade ‘n Tech Dispatch can be found at chinaus-icas.org/icas-trade-technology-program/tnt-dispatch/.

Soybeans have become a heated topic in the recent U.S.-China trade negotiations. After a 5-month halt in soybean purchase from the U.S., China placed its first order of the season on October 29. The long halt put significant economic pressure on U.S. soybean farmers, causing them to pressure the Trump administration for supportive actions. It is not the first time China reduced its soybean purchases from the United States. A similar halt of soybean trade occurred in 2018 during the height of the U.S.–China trade war in Trump’s first term, in which the trading volume and futures of U.S. soybeans dropped significantly. The reemergence of this problem illustrates that the underlying market and policy dynamics between China and the United States have not fundamentally changed...

In One Sentence

Mark the Essentials

Keeping an Eye On…

Say what you will about President Trump’s Liberation Day tariffs and his unilateral approach to trade policy, there can be no denying that he is getting his way – or, in his words, ‘winning’. The trade agreements that he signed in Southeast Asia this week with Malaysia and Vietnam are a perfect example.

At the APEC summit in November 2017 in Danang, Vietnam, during his first swing through the region as president, Trump had observed that he would “make bilateral trade agreements with any Indo-Pacific nation that wants to be our partner and that will abide by the principles of fair and reciprocal trade. What we will no longer do is enter into large agreements that tie our hands, surrender our sovereignty, and make meaningful enforcement practically impossible.” He had called it his “Indo-Pacific dream” at the time, although most Southeast Asian leaders would liken it to being an Indo-Pacific nightmare. Whether a dream or a nightmare, Donald Trump 2.0 has begun to accomplish exactly what he set out to do eight years earlier. The deals this past week are bilateral, obtained under duress of tariffs, heavily tilted in Washington’s favor, do not involve third party enforcement, and even include invasive terms that impinge on the counterpart’s sovereignty, such as Washington’s right to exit from the trade deal if that counterpart country enters into a trade “agreement with a country (China) that jeopardizes essential U.S. interests.” The issue of transshipment/rules of origin/Chinese intermediate goods content seems to be the lone knotty issue that still remains to be ironed out.

Over across in the U.S.-China negotiations, it is déjà vu time once again. The fifth round of talks in Kuala Lumpur was, in many ways, a rehash of the earlier Geneva (May) and London (June) rounds of talks. In Kuala Lumpur, as was the case in Geneva and London, the focus was on restoring a truce on the export controls front so that a pathway could be cleared for the larger trade and market access negotiations.

In Geneva, the U.S. had obtained a six-month commitment from China to facilitate the flow of export-controlled rare earth elements (REEs), following the placement by China of seven (of 17) REEs on its “restricted” export control list on April 4. China had export-controlled the REEs in response to the April 2nd announcement of ‘Liberation Day’ tariffs as well as placement of Chinese parties in the advanced IC, quantum computing and AI sectors on the U.S’ Entity List. Both sides also suspended part of their tit-for-tat tariffs – the U.S., by 24%; China, by 10%. In London, the two sides fixed their disagreement on the (slow) flow of Chinese REEs and magnets and agreed on a plan to ease reciprocal export controls. The disagreement had stemmed from China’s displeasure of a U.S. Commerce Department Guidance against the use of Huawei’s Ascend series chips, just one day after the Geneva meeting. Following the speeding-up of issuance of rare earth export licenses, Washington released its own hold on China-bound chip design software, jet engine parts and components, and ethane shipments. The administration also reversed course and licensed Nvidia and Advanced Micro Devices (AMD) to sell their export-controlled H20 and MI308 AI chips, respectively, to Chinese buyers.

This time around in Kuala Lumpur, and much like the earlier Geneva and London meetings, the U.S. once again obtained a commitment from China to both: (a) pause the implementation of its newest REE export controls for a year, and (b) facilitate the flow of existing export-controlled REEs, following Beijing’s bombshell October 9th announcement adding five new REEs to its export controls as well as the significant widening of its export controls net to capture a larger number of rare-earths related dual-use transactions. The Oct 9th announcement was in response to the U.S. Commerce Department’s late-September ‘50% Affiliates Rule’, which had swept hundreds, if not thousands, of Chinese enterprises into the U.S. Entity List. With a modus vivendi on export controls cemented, the ground was set for a Trump-Xi meeting.

The one-year pause – or, rather, truce – on the export controls front is the interesting wrinkle to emerge from Kuala Lumpur. It should effectively cover the period of Trump’s proposed state visit to Beijing – probably in early-February, as well as substantially cover the period leading into the APEC 2026 summit chaired by China and the 2026 G20 summit chaired by the U.S. The reciprocal presidential visits afford an action-forcing mechanism to strike, and begin implementing, a comprehensive trade deal on the lines of the January 2020 Phase One agreement – one which Trump craves. And which Xi has smartly dangled and utilized as a lever to check the U.S. from taking harsher export control measures. Nevertheless, whether the export controls truce – and détente in overall trade and tech ties – holds will be worth observing. Most probably, there will be ups-and-downs but the truce, and détente, should ultimately hold. Both sides have too much invested in its success – for Trump, a comprehensive trade agreement with mouth-watering market access; for Xi, damage minimization on U.S. export controls front.

Expanded Reading

China has had an export control regulation on dual-use items since 1997 based on its Foreign Trade Law, and issued its first Catalogue of Technologies Prohibited or Restricted from Export as early as 1998. Both were updated only intermittently…until five years ago.

Export Control Law (ECL) – In October 2020, China enacted the ECL as its foundational law to regulate dual-use items as well as streamline the various control lists strewn across government agencies. That streamlining was formalized in October 2024 with the promulgation of the Dual-Use Export Control Regulation, which took effect on December 1, 2024. The Dual-Use Export Control Regulation introduced two control lists: a “Watch” list and a “Restricted” list, with the latter being most similar to the U.S.’ Entity List. At this time, there are about 80 designated entities in the “Restricted” list, most of which are U.S. aerospace and defense contractors, as well as one U.S. drone manufacturer.

The regulation contains an extraterritorial dimension, which can be enforced when dual-use items manufactured outside China are mixed with specific dual-use items originating in China or dual-use items manufactured outside China use specific technologies originating in China. The former bears resemblance to the U.S. Commerce Department’s de minimis rule while the latter bears resemblance to the foreign direct product rule (FDPR). Both features were pressed into service in the October 9th announcement to control the export of dual-use rare earths and magnets, and related technologies. For added measure, the U.S.’ “50% Affiliates Rule” was replicated too. To be clear, China had already designated certain critical minerals including rare earths as dual-use items in late-2024 and early-2025 in response to President Trump’s ‘Liberation Day’ announcement in early-April, but it had not applied the extraterritorial dimension to earlier dual-use control announcements.

Catalogue of Technologies Prohibited or Restricted from Export

Starting in 2023, China’s Ministry of Commerce has proactively expanded the Catalogue, such that it lists over 125 items (including know-how and processes). The most famous listing was “personalized information recommendation technology” in August 2020, on the basis of which TikTok’s algorithm was placed on the Catalogue’s “restricted” list (and which President Xi has now recently agreed in principle to license). The other notable listing, and which now requires a license for export, is technologies related to the processing of lithium and other minerals for EVs and batteries.

Other Countermeasures Statutes

Unreliable Entity List (UEL) – The UEL was announced in 2019 and Regulations promulgated in September 2020. Today, there are about 70 entities designated on the UEL. While most are Taiwan-linked U.S. defense contractors, a U.S. medtech firm (Illumina, due to its lobbying for anti-China sanctions), an apparel firm (PVH Group, for discriminating against Xinjiang-originating products) and a U.S. subsidiary of a Korean shipping firm (Hanwha Shipping, also for lobbying) are on the list too.

Anti-Foreign Sanctions Law (AFSL) – The AFSL was originally enacted in June 2021 to deter compliance with unilateral laws and regulations applied by third countries, what Beijing calls “long-arm jurisdiction” against Chinese entities. It was meant to serve as a ‘blocking statute’ to protect Chinese entities but also included within its remitted foreign-invested entities in China, to warn them of the consequences in the China market of complying with foreign anti-China sanctions. More recently, the AFSL has been used to sanction individuals deemed to have supported conduct that endangered China’s ‘sovereignty, security or development interests’. Implementing regulations were promulgated in March 2025, and sanctions typically include asset freezes, visa bans, and restrictions on import/export activities. As of today, there are over 70 entities and over 100 individuals sanctioned under the AFSL. While most are Taiwan-linked U.S. defense contractors, prominent other sanctioned persons include U.S. Members of Congress, including Nancy Pelosi for her visit to Taiwan as House Speaker, U.S. non-government entities, such as the Reagan Library for hosting the Taiwanese President, EU political bodies such as EU Parliamentarians (since delisted), and think tanks for facilitating Xinjiang-related human rights sanctions.

Unjustified Extraterritorial Measures Regulation – The Regulation was issued by MOFCOM in January 2021, but it has mostly been superseded by/subsumed within the UEL and the AFSL.

As a general rule, foreign entities tend to be designated first to the AFSL and/or the UEL, before being placed in the Export Controls Regulation’s control lists. Given the regulation’s extraterritorial dimension, placement could lead to the denial of access to even trace amounts of Chinese intermediate products or technologies.

Legislative Developments

Hearings and Statements

Expanded Reading

Soybeans have become a heated topic in the recent U.S.-China trade negotiations. After a 5-month halt in soybean purchase from the U.S., China placed its first order of the season on October 29. The long halt put significant economic pressure on U.S. soybean farmers, causing them to pressure the Trump administration for supportive actions. It is not the first time China reduced its soybean purchases from the United States. A similar halt of soybean trade occurred in 2018 during the height of the U.S.–China trade war in Trump’s first term, in which the trading volume and futures of U.S. soybeans dropped significantly. The reemergence of this problem illustrates that the underlying market and policy dynamics between China and the United States have not fundamentally changed.

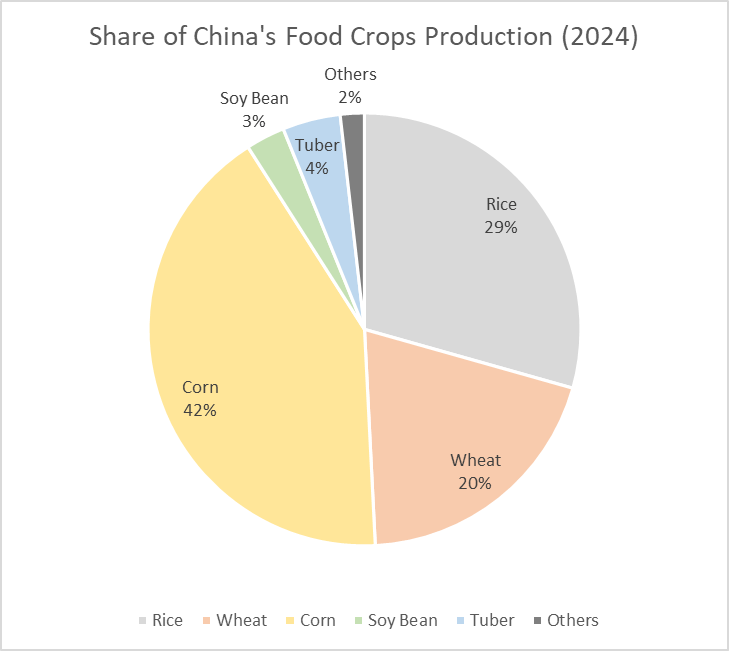

China’s geological limitations, population, and history all contribute to its high demand for soybeans. China must feed about 17% of the world’s population with only 11% of the world’s arable land. Historically, this imbalance of population and farmland has made China largely reliant on food imports to feed its population, and the country has worked hard to change the status quo in the past 70 years. Ensuring food security has always been a critical national priority for China. In October 2019, China released a White Paper titled Food Security in China that emphasized self-sufficiency of grains, particularly rice, wheat, and corn. This leads to a preference for those crops when domestic agricultural land is limited and scarce to maximize domestic food output. Nowadays, China produces enough grains to fulfill around 95% of its own demand, and its output of rice and wheat is able to fully meet its domestic needs.

Although China is able to reach self-sufficiency on grains, this is not the case for soybeans. Soybean is not a grain, and is not a major share of Chinese citizens’ daily diet. This means the legume has a lower planting priority when deciding what crop to plant, accounting for only 3% of China’s total food crop output. It is used primarily for animal feed, especially for raising pigs and chickens. The nation’s rising meat consumption has driven a constant surge in demand for soybeans used as animal feed. China not only needs to feed its people with plants, but also meat. The country is the world’s largest producer and consumer of pork, resulting in a huge, growing need.

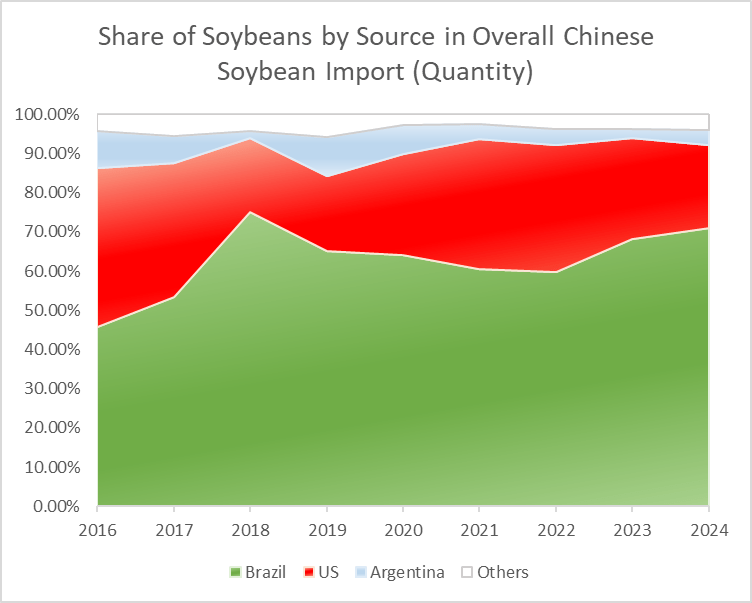

Brazil is the largest soybean producer globally, accounting for roughly 41% of world production, followed by the U.S. at about 28%. China’s previously mentioned planting priorites and large pork industry make it the world’s largest consumer of soybeans, accounting for around 62% of global soybean imports in the past five years. As such, global production is largely shaped by China’s demand patterns — China’s demand is the world’s demand.

Brazil’s rise as China’s main soybean supplier was not only a result of tariffs but also of favorable seasonal and logistical conditions. Brazil’s harvest season complements that of the U.S., allowing Chinese buyers to maintain year-round supply. In addition, Brazil’s southern ports provide direct shipping routes to China’s coastal regions, making it a convenient alternative when trade tensions with the U.S. escalate.

After China joined the World Trade Organization in 2001, its soybean imports from the U.S. rose dramatically. American producers supplied high-quality beans efficiently through advanced logistics systems, and the U.S. quickly became a major supplier for China’s growing feed industry. The interdependence was mutually beneficial: China gained a stable source of feed for its expanding livestock sector, while American farmers secured a reliable and lucrative export market.

Soybeans are America’s second-largest planted crop, accounting for about 32% of total agricultural acreage, just behind corn at 33%. American farmers have long expected to sell a large share of their soybeans to China, even without formal long-term trade agreements. Over the past five years, China has purchased more than half of all U.S. soybean exports, making it the single largest buyer. This heavy dependence means that when China halts its purchases, U.S. farmers face serious oversupply problems and collapsing prices. The American soybean industry has therefore become deeply vulnerable to disruptions in trade relations with China.

After the White Paper, China focused on diversifying and derisking its food supply chains to avoid over dependence on a single source, redirecting more of its purchases from the U.S. to Brazil. This diversification weakened the previously dominant U.S. role in China’s soybean supply. Prior to this year, the U.S. experienced the least amount of soybean exports to China in 2018 and 2019. The 2018–2019 U.S.–China trade war marked a turning point for global soybean trade. China’s retaliatory tariffs on U.S. soybeans caused exports to plummet and prices on the Chicago Board of Trade to become highly volatile. The U.S. government responded with the Market Facilitation Program, a multibillion-dollar subsidy package intended to compensate farmers for their losses. This time, the Trump administration is bringing the topic to the trade negotiations. These measures underscored the political importance of the soybean industry in U.S. domestic politics, particularly in agricultural states that are typically supporters for the Republican Party.

China’s purchase halt this harvest season exerted increasing costs on American soybean farmers for storage of unsold soybeans that were already harvested. U.S. Treasury Secretary Bessent claimed on October 26 that China has agreed to buy a “substantial” amount of American soybeans after talks with Chinese counterparts. The history of soybean trade between the two countries mirrors the broader political and economic cycles of cooperation, tension, and realignment in U.S.–China relations. Every shift in political rhetoric or trade policy immediately influences future markets, demonstrating the fragility of an export model built on a single dominant buyer.

Soybeans are not just an agricultural commodity; they are a strategic instrument in economic diplomacy. For the U.S., soybeans carry significant political weight. The agricultural sector is a crucial part of America’s economy and plays an important role in elections, plus farm incomes depend heavily on exports. The Trump administration’s tariff policies and subsequent subsidies highlighted how agricultural trade can influence voter sentiment and policy decisions. As a result, soybeans have become a symbolic battleground in U.S.–China relations: a product where trade, politics, and national strategy intersect.

The soybean trade between China and the U.S. goes beyond the economics of crops and commodities. China’s demand for soybeans remains unmatched globally. Yet, a fundamental imbalance persists: China can stop buying from the U.S. and turn to alternative suppliers, but the U.S. cannot easily find an alternative market to replace China. It captures the complexity of globalization, dependence, and strategic maneuvering between two of the world’s most powerful economies. As trade negotiations continue, soybeans remain both a symbol and a tool of leverage in a relationship that shapes not only agricultural markets but also the geopolitical landscape of the twenty-first century.

This issue’s Spotlight was written by Yunchao Mao, Reserach Assistant Intern.