Gulf exporters are scrambling to bypass the Strait of Hormuz after Iran choked off most of the maritime traffic in one of the world’s most critical energy corridors. Saudi Arabia and the United Arab Emirates rushed to divert exports through overland pipelines; officials

warned that even naval escorts could not guarantee safe passage. About a fifth of the world’s oil and liquefied natural gas (LNG) trade passed through this narrow waterway.

The immediate shock was felt in the Gulf. The strategic aftershock is being felt much farther north.

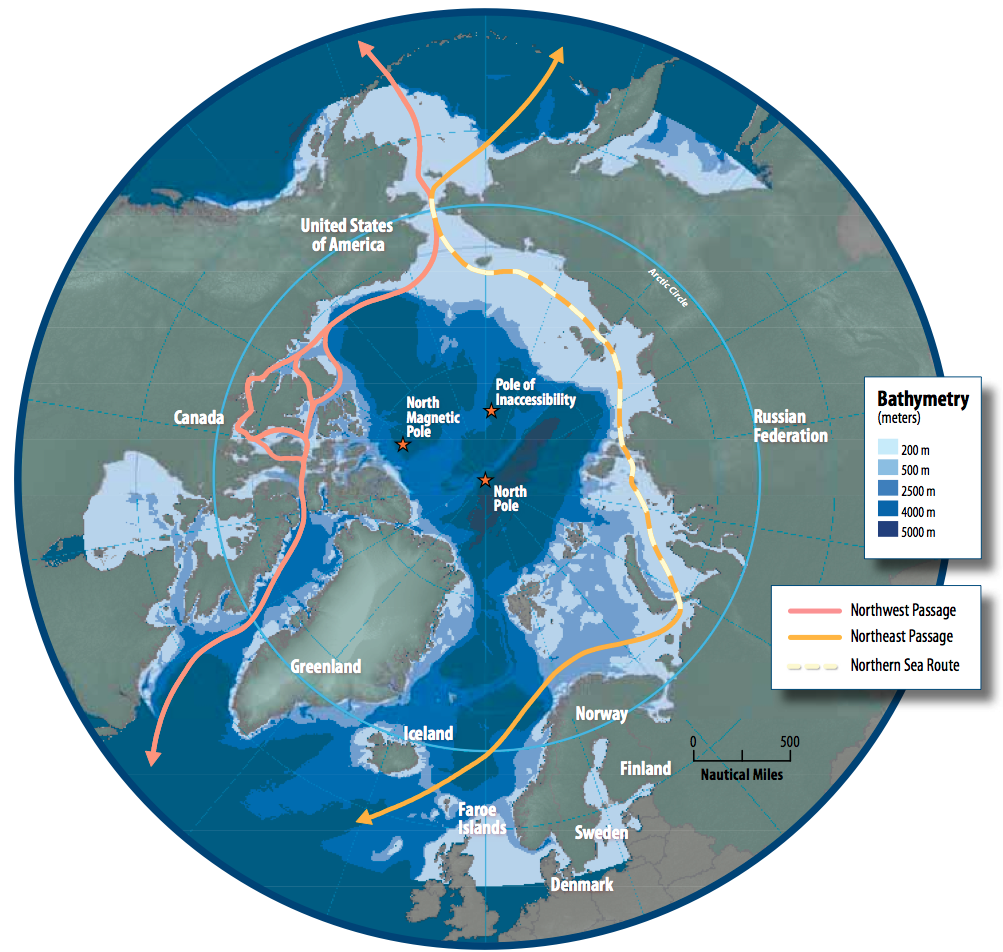

That shift is visible in Alaska. The US-backed

Alaska LNG project now aims to finalise investment decisions on the pipeline this year and on the export terminal early next year, with first exports by 2031. With planned capacity of 20 million tonnes a year and preliminary commitments covering about 13 million tonnes, the project is gaining fresh momentum. Importantly, Alaska offers something Gulf suppliers cannot: direct access to North Asia without passing through Hormuz.

That matters, especially for Japan, South Korea and other Asian importers. JERA, Japan’s largest power generator, has said Alaska offers proximity to Asian demand centres and access to long-stranded large gas reserves, helping to support regional

LNG supply security. Alaska LNG, in other words, is no longer just a commercial proposition. With instability in the Middle East, it is increasingly being reframed as an energy security asset.

But the Arctic windfall is not confined to the United States. Russia’s Arctic LNG, though sanctioned, has not been pushed out of the market altogether; part of it is

continuing to shift towards Asian buyers. If the US is gaining from the security premium attached to a newly revalued project, Russia’s Arctic resources are also mattering more as a means of sustaining exports and economic resilience under pressure.

As the world places greater weight on resource security and shipping routes, the importance of Russia’s Arctic assets

may increase – even as that importance remains constrained by sanctions and external pressure.

Other Arctic actors are benefiting too, but not in the same way. For Norway, the gain lies less in a sudden export surge than in the rising strategic value of its

existing supply. Oslo has not stepped back from Arctic hydrocarbons: it has expanded its licensed oil and gas exploration blocks to 76, including 68 in the Barents Sea. But the upside is capped by capacity. Norwegian energy giant Equinor recently said it had no spare oil and gas capacity left to bring to market.

Norway’s Arctic gain, then, is not about ramping up supply so much as about the security premium attached to what it already produces.

Greenland points to a different kind of Arctic gain. Its decision to stop issuing new oil and gas exploration licenses in 2021 does not make it irrelevant to the new strategic picture. As governments across the world place greater emphasis on supply-chain diversification and critical minerals, Greenland is more likely to benefit from the rising value of strategic resources than from hydrocarbons.

Canada’s gains are even more indirect, reflected less in hydrocarbons than in the growing importance of northern infrastructure, critical mineral development and high-latitude resource security.

The next question is whether this shifting landscape will eventually bring countries back into some form of cooperation with Russia, despite the war in Ukraine. The answer will not be a simple yes or no. It will be fragmented.

In Europe, the political and legal barriers remain high. The European Union has formally adopted a

stepwise ban on Russian pipeline gas and LNG imports, with LNG imports to be fully prohibited from the beginning of 2027, and pipeline gas from autumn 2027. European Commission President Ursula von der Leyen has warned that returning to Russian fossil fuels would be a “strategic blunder”. Europe is therefore unlikely to return any time soon to the energy relationship it once had with Moscow.

Yet the pressure to revisit that position has not disappeared. Belgian Prime Minister Bart De Wever recently argued that Europe should restore relations with Russia to regain access to cheaper energy. His remarks triggered an immediate backlash but also suggest any future Russia-related energy cooperation will be marked more by divergence than convergence: Europe will continue shrinking its ties, while Asian markets and some non-Western actors may still leave room for selective engagement.

None of this means the Arctic can replace the Gulf. It means, instead, that instability in one energy centre raises the strategic premium on alternatives elsewhere.

This, ultimately, is the real meaning of the Arctic’s windfall. The region is not suddenly becoming richer. Rather, the world is rediscovering that when traditional energy centres become less stable, high-latitude resources, shipping routes and infrastructure gain strategic weight.

The Arctic is no longer just a distant arena of climate change and regional governance; it is increasingly a frontier where energy security, supply-chain restructuring and great-power competition meet. Those who can turn resource advantages into more secure supply, stronger infrastructure positioning and greater strategic influence will hold the edge in the next phase of global competition.

For major energy consumers,

including China, the issue is not whether to chase an Arctic windfall, but whether they understand the deeper shift under way. The Gulf may remain the world’s energy centre of gravity, but as geopolitical risk spreads, the strategic value of the high north will only keep rising.

This commentary was originally published in SCMP on March 25, 2026.

The Bering Strait: Managed Openness at the Arctic Gateway