U.S. Trade Representative Katherine Tai testifies before the Senate Appropriations Subcommittee on Commerce, Justice, Science, and Related Agencies during a hearing on the proposed budget for fiscal year 2022 for the Office of the U.S. Trade Representative on Capitol Hill on April 28, 2021 in Washington, DC. (Photo by Sarah SilbigerGetty Images)

Resident Senior Fellow

On October 4, United States Trade Representative (USTR) Katherine Tai unveiled the outlines of the administration’s emerging “new approach” on trade policy towards China. Truth be told, the new approach appears awfully similar in substance, although not in tone, to her predecessor’s approach.

USTR Tai made two overarching points. First, that trade and tariff policy is a component of the administration’s broader worker-focused agenda, and trade policy will be taking a relative backseat until the administration’s infrastructure-building, competitiveness, and worker training agenda had been put into motion. Second, that the U.S. did not seek to decouple from China but would rather insist on reframing the terms of its ‘recoupling.’ She expressed skepticism, though, of China’s willingness to make the necessary structural reforms.

On the immediate trade and tariff policy challenges concerning China—future of the Phase One trade agreement; negotiation of Phase Two ‘structural’ issues; readjustment of Section 301 tariffs; ‘architecture’ of USTR’s engagement with Chinese counterparts, etc.—USTR Tai left more unsaid than said. And to the extent that clarity was provided, it bore more in common than it differed from the Trump administration’s policies.

There is apprehension within U.S. business that some of the Section 301 tariffs on China might become permanent. This would be economically harmful and politically damaging to the bilateral trading relationship. A WTO arbitral panel has also ruled these tariffs to be illegal. USTR Tai’s constricted focus on trade enforcement and inability to spell out an agenda of regional and multilateral trade liberalization is just as concerning.

USTR Tai’s less-than-compelling policy vision masks a troubling dimension of American trade politics: with the Republican Party—hitherto a relative bastion of free trade thinking—bending to ex-President Trump’s economic nationalist will, the Beltway’s decades-old, pro-trade consensus might get increasingly shot through with streaks of protectionism.

On October 4, following a months-long inter-agency China policy review, United States Trade Representative (USTR) Katherine Tai unveiled the outlines of the administration’s emerging “new approach” on trade policy towards China in an eagerly anticipated speech in Washington, D.C. The USTR-led China policy review was the first of its kind in more than 15 years.

In her remarks, USTR Katherine Tai made several overarching points.

First, the Biden administration does not seek to decouple from China. Decoupling is unrealistic and not in the United States’ interest. The U.S.-China economic debate needed to be framed rather as the terms on which the two economies should be recoupled. In the next breath however, she expressed skepticism of China’s willingness to make the necessary structural changes to its trade and industrial policy regime in order to satisfy Washington. “Beijing has doubled down on its state-centered economic system…[and] China’s plans do not include meaningful reforms,” she noted. USTR Tai’s view is not an uncommon one in Washington, D.C. At the same time, the view fails to square with the reality that China has concluded negotiations with the European Union on a high-quality Comprehensive Agreement on Investment (CAI) and has submitted its candidature for membership to the gold-standard Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) agreement. The CAI and CPTPP are indicators of China’s reformist inclination, not an indicator to the contrary.

Next, USTR Tai remarked that the Biden administration’s trade and tariff policy China, as well as other trading partners, was a component of the administration’s broader economic agenda. What is best for American workers and interests would dictate her trade policy agenda. Presumably, concerted attention to trade and tariff policy will take a backseat until the administration’s infrastructure-building, competitiveness, and worker training agenda—‘investments’ that are included in President Biden’s Build Back Better plan—has been put into motion. Concerningly, she did not rule out the use of tariff-based protectionist measures to defend the interests of American workers; to the contrary, she left the door open for a future round of tariff-raises.

Third, USTR Tai observed that her foremost trade policy priority, going forward, would be to focus on trade enforcement. “Above all else, we must defend—to the hilt—our economic interests…[and] be prepared to deploy all [trade enforcement] tools and explore the development of new ones” she intoned. However, there was nary a mention of the words ‘regional and multilateral liberalization’ in her speech. Trade enforcement is all fine and dandy; nobody is ever against it. But without trade enforcement being married to a meaningful strategy of trade liberalization, it essentially amounts to a ‘one-step-forward-two-steps-back’ policy of soft protectionism.

Finally, in order to elicit—or rather coerce—meaningful reform out of China, the U.S. intends to work closely with its European allies and like-minded partners to build a “truly fair international trade [regime] that enables healthy competition.” This comports with the overall a la carte ‘Allies First’ approach of the Biden administration contrasted with the Trump administration’s ‘America First’ philosophy. Left unsaid by USTR Tai, however, was an elaboration of how the gap between the two sides’ views on trade and economic matters with China would be managed. The European Union and Japan wish to tether China’s industrial subsidies and state-owned enterprises-related structural reforms to multilateral rulemaking. The U.S., on the other hand, would much prefer that these disciplines are imposed and enforced within a narrower bilateral, trilateral or small group setting.

In addition to these points, USTR Tai touched on a number of more immediate trade and tariff policy challenges concerning Beijing. These include the future of the Phase One trade agreement, negotiations towards a Phase Two ‘structural’ issues agreement, readjustment of the existing Section 301 tariffs, and the format of USTR’s engagement with Chinese counterparts. On each of these points, USTR Tai left more unsaid than said. And to the extent that clarity was in fact provided, it resembled an approach more in common with her predecessor Robert Lighthizer’s criticized approach towards China than a new or original gameplan.

Overall, USTR Katherine Tai’s advertised “new approach” on China trade policy is not terribly different from the broken “paradigm” of the previous administration’s approach. This is arguable despite her castigation of the Trump team for its failure to “meaningfully address the fundamental concerns that [Washington has] with China’s trade practices and their harmful impacts on the U.S. economy.” Just as before, tariffs are to be leveraged to elicit changes in China’s behavior (despite ample evidence of the self-defeating nature of Trump’s Section 301 tariffs). Unilateralism is not jettisoned but is to be leavened with a more “allies first” approach. And, just as before, adherence to multilateral trade law is to be approached with an a la carte attitude—picked, chosen and harped upon when convenient to advance American economic interests; kicked into the long grass when politically inconvenient.

The remainder of this Issue Brief is drawn up in the context of USTR Katherine Tai’s unveiling of the outlines of the administration’s emerging trade and tariff policy approach vis-à-vis China. In Section I, the Issue Brief carries a prescient Insider Interview with the President of the U.S.-China Business Council, Craig Allen, on all matters China trade and tariff policy considered. Issue Brief concludes in Section II with a summarized backstory of how Washington and Beijing arrived at their current dismal state of trade policy affairs, levying self-damaging tit-for-tat tariffs across a wide range of goods. If the “durable coexistence” that USTR Tai alluded to in her delivered remarks is to take hold in U.S.-China relations, it is as important to look backwards at this recent history as it is important to look ahead and chart a path forward.

This Insider Interview was conducted on September 21, 2021 by telephone. Answers below are paraphrased summaries of Amb. Allen’s responses.

What is the rough timeline for USTR’s completion of its China Policy Review, and timeline for concerted reengagement subsequently with Chinese counterparts?

USTR continues to work its way through its China trade policy review. It is anticipated that it will be completed soon…and certainly in the not-too-distant future. USTR understands it needs to bring its China policy review to a conclusion, given that U.S. business and other important stakeholders are getting anxious because of the slow pace of completion of the review. There are three action-forcing dates that are putting pressure on USTR to conclude the review. The first is the U.S.-EU Trade and Technology Council (TTC) meeting due to be held in Pittsburgh on September 29. It would be useful for USTR to have its review concluded by then, so that notes can then be exchanged with the Europeans on how the U.S. and EU could coordinate trade and technology policy regarding China. The second action-forcing date is the G20 meeting towards the end of October. And the outer deadline for concluding the review should be November 13. On that day, President Joe Biden is due to address the APEC CEO Summit (being chaired virtually by the host, New Zealand). It would be essential that Mr. Biden have his China—and Asia—trade, tariff and investment policies lined up by that date. Furthermore, with the U.S. hoping to host APEC in 2023, clarity on these issues as well as a positive workplan for region-wide engagement and hopefully liberalization would be beneficial.

At this time, there is continuing mid-level engagement by USTR with the Chinese side; particularly on the Phase One market purchases issue. But there has not been sustained high-level engagement. Such high-level engagement needs to happen soon. And it must happen before the end of the year because the detailed Phase One market purchase targets expire at the end of the year. USTR needs to have a detailed plan in hand on how it plans to engage the Chinese side going into 2022, 2023 and beyond.

Finally, from a procedural or process standpoint, there seems to be no clear direction yet within the Biden administration on the mechanism or framework within which it plans to engage the Chinese side. During the Obama administration, there was the Strategic and Economic Dialogue (S&ED) co-headed by the Secretary of State and the Treasury Secretary. During the latter years of the Trump administration, there was the Trade Framework Group (TFG) headed by USTR and co-chaired with the Treasury Department. The Biden team does not seem to have arrived at a decision on this point. This having been said, it was not helpful that Vice Premier Liu placed separate calls to USTR’s Tai and Treasury’s Yellen earlier this summer. It would have been better if the two had been on a joint call together with Vice Premier Liu. This episode also goes to show that, at least at this point in time, there is a degree of interagency coordination on China lacking at the U.S. end.

What seems to be USTR’s plan of action going forward on the Section 301 and Sections 232 steel tariffs (insofar as latter pertain to China), and are these tariffs to be accorded differing treatments (say, some 301 tariffs rescinded; China 232 tariffs maintained)?

The U.S.-EU Trade and Technology Council is due to meet in Pittsburgh on September 29. Among the issues to be hopefully discussed also are the Section 232 steel tariffs that have been imposed by the U.S. not only on China but also on the EU. How the Biden administration deals with this tariff issue regarding the Europeans will provide an early inkling of its strategy on the Trump-era tariffs. Hopefully, these steel tariffs, which burden downstream producers and consumers, will be readjusted. This having been said, the Section 232 steel tariffs imposed on China are more connected to the multilateral (OECD-led) discussions related to overcapacity in the steel sector. So, any reduction or removal of the China steel tariffs would be contingent on progress in these OECD-led overcapacity talks, and therefore USTR’s strategy on readjusting steel tariffs vis-à-vis China could be quite different from its strategy on readjusting steel tariffs vis-à-vis the Europeans.

Regarding the Section 301 tariffs imposed on China, there unfortunately seems to be no rush to remove them. There is even a danger that some of the tariffs, which have been imposed on a wide range of goods, could become permanent. This would be economically harmful to consumers in the United States and very damaging to the bilateral trading relationship. So at present, the bottom line is that there is not only no clarity on which tariffs might or might not be reduced or withdrawn but also a chance that some of these tariffs might not get reduced or withdrawn at all—. As a first step, the business community has requested that the exclusions (to the tariffs) that USTR had permitted on certain imported products should be extended. On September 16, China extended its exclusions from the tariff countermeasures on U.S. imports that it had imposed, and USTR, too, at minimum should extend the tariff exclusions at its end.

What is USTR’s view of the state of Phase One compliance, and is there a push to extend out the market purchase commitments beyond 2022?

The Phase One issues is a two-part story—part one related to the policy elements, and part two related to the market purchase commitments in the agreement. On part one, the Phase One policy elements, the story is a good one. There were several detailed commitments related to IP protections, technology transfer, agricultural biotechnology, financial services liberalization, and currency, and China has substantially—although not entirely—fulfilled these commitments. China’s scorecard is a good one, and there is satisfaction at the U.S. businesses end on the Phase One policy elements implementation.

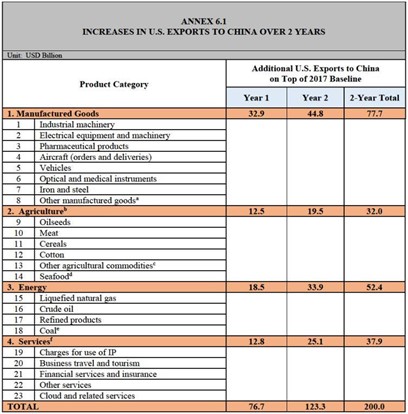

On part two, the Phase One market purchase commitments, the story is much less positive. In Year One of implementation, China was to purchase $77 billion of goods and services more than the 2017 U.S. export baseline. And in Year Two of implementation, the target was to be $123 billion more than the 2017 baseline. The reality is that U.S. exports to China today are more-or-less at the 2017 baseline and, therefore, almost 40% behind target. There is an understanding both at the USTR and within the Biden administration that COVID-19-related economic disruptions have set back the attainment of these purchase commitments. But at the same time, there is also a degree of unhappiness that some of the falling behind on targets is due to MOFCOM regulatory changes that has made it harder to export U.S. goods into China. At the end of the day, the market purchase targets are written commitments by China. As such, China must continue to make best possible efforts to honor these purchase commitments.

As to what follows next after the detailed purchase commitment targets expire in December 2021, there is an eerie silence on this topic at USTR. Perhaps the Biden administration is not keen to utilize the framework that a predecessor (Trump) administration had laid out. But on the other hand, the Biden administration has not articulated an alternative mechanism or plan. The thinking within the U.S. business community is that the market purchase commitments will be extended out into 2022 and 2023 by the Biden administration before they expire at the end of December (2021). But there is no certainty that this will be the case; at least at this point of time. And this is adding to unease within certain segments of American business, especially among U.S. ranchers and farmers of bulk commodities like corn and soybeans, for whom the China market has been very profitable.

How is USTR planning to approach the structural Phase Two issues with China – engage China directly on this issue first (and fairly soon) OR engage China only after a possible Section 301 investigation has been completed and common policy position lined up with the EU and Japan?

The Biden administration’s approach on a Phase Two negotiation on the ‘structural’ economic issues with China is by no means set in stone. It is, in fact, very much at a stage of review and deliberation. After all, the Biden administration is actively supporting the passage of the U.S. Innovation and Competition Act (USICA) on Capitol Hill, and USICA involves disbursing significant subsidies to emerging and strategic industries in the U.S. As such, the administration’s immediate focus is on the substance and method of industrial subsidization policy at home; not on subsidization practices overseas, to which it will turn its attention to later—but soon. Additionally, it becomes hard to complain about mechanisms of subsidization in China if the United States’ own practices depart from global norms and rules. It is not clear that this departure will in fact be the case…but it is also still too early to confirm that it will not. In any case, this focus on restoring industrial competitiveness at home is for being the overshadowing focus on reigning-in China’s non-complaint practices in the area of industrial subsidies and, more broadly, industrial policy.

This having been said, the probability of the Biden administration initiating a new Section 301 investigation of China’s industrial subsidy and industrial policy practices is quite high. The more pertinent question to ask though is this: What exactly is to be known, and what is it that can be known, through this Section 301 investigation (aside from the investigation being a trigger for some sort of punitive action to follow after its conclusion)? The reason is this: It is common knowledge that, while China’s industrial subsidy practices do not comply with global norms and standards, these subsidy practices are shrouded in non-transparent disbursals that no amount of poking around in the context of a Section 301 investigation will be able to identify. At the end of the year-long investigation, USTR will probably be not much wiser on the scale, scope, mechanics, and fine-print of these subsidy practices which are couched in layers of non-transparent dealing at the Chinese end.

Therefore, the more useful pathway forward in this regard is for the U.S. to support its European and Asia-Pacific partners as they engage Beijing in investment liberalization-related discussions. In the Comprehensive Agreement on Investment (CAI) with China, the European Commission obtained useful industrial subsidy-related transparency commitments. The Commission should hold Beijing strictly to these provisions (if and when the CAI is ratified and enters into force). With China formally applying to join the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP) agreement, the U.S. should push its Asia-Pacific partners, too, to demand that Beijing display willingness to accede to and abide by the strict standards of the CPTPP’s state-owned enterprises (SOE) chapter. These negotiations—as well as utilizing the U.S.-EU Trade and Technology Council (TTC) as an internal discussion forum—provide a useful reframing mechanism to engage China on the Phase Two structural issues at a time when the Biden administration appears somewhat consumed at home on industrial subsidies and competitiveness-related legislation.

Nevertheless, engaging China in a dedicated bilateral format on the Phase Two ‘structural’ issues must become an imperative for USTR. The goal is not to obtain immediate results. Rather, the goal should be to get on the right track towards a common destination; one that features China’s embrace of level playing field rules and market-based, advanced country-consistent industrial and digital policy standards.

Candidate Donald Trump had campaigned on an unabashedly anti-China platform in 2016, listing the country as a key trade policy violator. In his Seven Point Plan to “Make America Great Again,” Candidate Trump promised to “use every lawful presidential power to remedy trade disputes if China [did] not stop its illegal activities, including its theft of American trade secrets.” He went on to list numerous statutory trade enforcement tools—Section 232 of the Trade Expansion Act of 1962; Section 201 of the Trade Act of 1974; Section 301 of the Trade Act of 1974—with which he would punitively sanction China. In keeping with his campaign promise, on August 24, 2017, the Trump administration initiated a Section 301 investigation of China’s alleged forced technology transfer policies and practices. Seven months later, on March 22, 2018, Trump’s United States Trade Representative, Robert Lighthizer, reported back with four damning findings pertaining to China’s practices related to forced technology transfer and non-market technology licensing requirements as well as the theft of sensitive commercial information and trade secrets from the computer networks of U.S. companies.

Pursuant to these findings, on the same day, President Trump issued a Presidential Memorandum which laid out a three-part course of follow-on action.

The Presidential Memorandum provided the basis for the imposition of the Section 301 tariffs on China—tariffs which continue to take effect to this day. The Memorandum was also a catalyst for an intense three-week period of Sino-American consultations in May 2018 to resolve the deep-seated trade, investment, and intellectual property rights-related differences. At their very first meeting, the U.S. side made eight far-reaching demands.

Sections 301-310 of Chapter 1, Title III of the Trade Act of 1974 grants the President broad authority to unilaterally suspend U.S. trade concessions or impose duties or other restrictions on the products or services of a foreign country that is “unjustifiable and burdens or restricts United States commerce.” The breadth of delegated authority that the President enjoys is immense. He/she is authorized to employ “any diplomatic, political, or economic leverage available” to remedy the unreasonable or discriminatory burdens imposed on U.S. commerce by a foreign government. Crucially, the statute does not require the trading partner to be in violation of the U.S.’ international legal rights in order to fall within the 301 dragnet. So long as its acts, policies or practices are “unreasonable”—unreasonable defined as any act, policy or practice which “while not necessarily in violation of, or inconsistent with, the international legal rights of the U.S., is otherwise unfair and inequitable”—it can be subjected to penalties.

The Section 301-10 enforcement tool is prima facie inconsistent with the multilateral and neutral third-party dispute settlement procedures envisaged under the WTO’s dispute settlement understanding (DSU). To ensure consistency between domestic statute and multilateral law, in September 1994, the Clinton administration pledged in a Statement of Administrative Action (SAA) to the U.S. Congress at the time of ratifying the Uruguay Round Trade Agreement that in Section 301 cases, the U.S. would allow WTO DSU procedures to run their course before any enforcement action would be taken. And that enforcement action would be consistent with the WTO’s dispute settlement ruling; it would not be unilaterally determined action. This approach was legally confirmed in WTO jurisprudence in January 2000 in a case brought by the European Union challenging the validity of the Section 301 tool.

On April 3, 2018, without so much as the holding of even a single WTO dispute settlement hearing, USTR Robert Lighthizer proposed that an additional 25 percent duty covering 1,333 tariff lines be applied to about $50 billion worth of Chinese exports to the U.S. The tariffs went into effect on July 6, 2018. A day after USTR Lighthizer’s proposed duties, China initiated a Request for Consultation at the WTO challenging the American measure. The Request stated that the U.S.’ proposed tariffs violated Articles I.1 and II.1(a) and (b) of the General Agreement on Tariffs and Trade (GATT) as well as Article 23 of the WTO’s Dispute Settlement Understanding (DSU).

On September 15, 2020, two-and-a-half years after the initiation of consultations, a WTO arbitral panel ruled that the U.S.’ tariff measures were inconsistent with each of the GATT articles that Beijing had listed out and had therefore violated China’s legal rights. The panel struck down the U.S. argument that the tariffs were “legally justified because they were necessary to protect public morals,” as reflected in standards of right and wrong related to China’s policies and practices of using coercion and subterfuge to improperly acquire intellectual property.” The panel ruled that USTR’s own Section 301 investigative reports had failed to mention the word ‘public morals’ even once, and furthermore the relationship between the chosen measures—additional duties applied to specified products—and the public morals objective being pursued was not explained. In December 2019, the Trump administration blocked the formation of a quorum to hear appeals cases at the WTO’s Appellate Body, ensuring that this Section 301 award remains for the time being consigned to the long grass.

First, the U.S. side demanded that China reduce its trade surplus by $100 billion within 12 months, beginning on June 1, and by an additional $100 billion over the following 12 months, such that the U.S. trade deficit with China will have decreased compared to 2018 by at least $200 billion by the end of 2020. China’s additional purchase of U.S. goods was to account for 75 percent of the first $100 billion reduction and 50 percent of the second reduction.

Second, on intellectual property rights, the U.S. side demanded that China scrap its support to industries listed in the Made in China 2025 plan as well as eliminate certain policies and practices with respect to technology transfer by January 1, 2019. Beijing was also asked to ensure that all Chinese government-conducted and sponsored cyber intrusions into U.S. commercial networks and cyber-enabled theft targeting U.S. companies be terminated.

Next, regarding Chinese investment in the U.S., the U.S. side demanded that China cease challenging, opposing or taking any retaliatory action even if the U.S. went ahead and restricted Chinese investments in sensitive U.S. technology sectors.

Fourth, regarding U.S. investment market access in China, the U.S. demanded that China issue an improved nationwide negative list for foreign investment by July 1, 2018. Within 90 days thereafter, the U.S. would identify existing Chinese investment restrictions that denied American investors fair, effective, and non-discriminatory market access and treatment. Following receipt of the U.S. list of identified investment restrictions, China was to act expeditiously to start removing the specified restrictions.

Fifth, regarding tariffs, the U.S. demanded that by July 1, 2020, China reduce its tariffs on all products in non-critical sectors to levels that were no higher than the levels of the United States’ corresponding tariffs. Specified non-tariff barriers were also to be removed—even as U.S. maintained the right to impose restrictions and tariffs on products in critical sectors identified in the Made in China 2025 plan.

Sixth, the U.S. demanded that China improve market access for U.S. services and service suppliers.

Seventh, similarly China was to improve market access for U.S. agricultural products.

Finally, from an implementation standpoint, the U.S. demanded that the two sides meet on a quarterly basis and review the proposed targets and reform commitments. If China did not comply with its assigned targets in a time-bound manner, then the U.S. would be at liberty to impose additional restrictions and tariffs on Chinese exports.

July 6, 2018 A first tranche of 25 percent tariffs on $34 billion in Chinese imports goes into effect.

August 23, 2018 A second tranche of 25 percent tariffs on $16 billion in Chinese imports goes into effect.

September 24, 2018 A third tranche of 10 percent tariffs on $200 billion in Chinese imports goes into effect. The rate increases to 25 percent on May 10, 2019, following the breakdown of the 90-Day Trade Truce negotiations.

September 1, 2019 A fourth tranche of 15 percent tariffs on $120 billion in Chinese imports goes into effect. Another round of 15 percent tariffs on $160 billion of Chinese imports, which was to go into effect on December 15, 2019, is suspended.

The May 2018 negotiations could not be brought to a successful conclusion, leading to the imposition of a first tranche of tariffs on July 6, 2018. Chinese counter-tariffs followed soon thereafter. In total, four rounds of tariffs on Chinese imports were imposed by the Trump administration. The remarkable feature of the eight demands issued nonetheless in May 2018 is that they foreshadowed many identical demands in the Phase One Economic and Trade Agreement signed by the two sides on January 15, 2020. The Phase One agreement contains six substantive chapters listing a plethora of detailed commitments ranging from IP protections, technology transfer, agricultural biotechnology regulations, financial services liberalization to currency and exchange rate matters. At its heart though is a detailed set of market purchase commitments that China was obliged to fulfil over a two-year period. Specifically, in Year One of implementation, China was to purchase $77 billion of goods and services in excess of the 2017 U.S. export baseline. And in Year Two of implementation, the target was to be $123 billion in excess of the 2017 baseline. Totally, over the two-year period starting January 1, 2020, China’s imports of covered goods and services from the United States was to exceed the corresponding amounts imported in 2017 by no less than $200 billion.

Following the signing of the Phase One agreement in January 2020, the United States agreed to reduce the tariffs on items listed in the fourth tranche of exporters from 15 to 7.5 percent, effective February 14, 2020. The 25 percent tariffs on approximately $250 billion of Chinese imports listed in tranches 1-3 continue to remain in effect (although with product specific exclusions granted to U.S. importers). The Trump administration was also able to get China to agree to eliminate the retaliatory tariffs that it had imposed targeting the U.S. agriculture sector.

As of late-Summer 2021, China remains almost 40 percent off its 2021 import purchase targets. As per the closely watched U.S.-China Phase One Tracker put out by the Peterson Institute for International Economics, through August 2021, U.S. exports to China of overall covered products were $70.6 billion compared with a year-to-date target of $113.0 billion, or 62 percent of the year-to-date target. For covered agricultural products, through August 2021, U.S. exports were $17.9 billion compared with a year-to-date target of $20.0 billion, or 89 percent of the year-to-date target. For covered manufacturing products, through August 2021, U.S. exports were $43.8 billion compared with a year-to-date target of $71.6 billion, or 61 percent of the year-to-date target. And for covered energy products, through August 2021, U.S. exports were $8.9 billion compared with a year-to-date target of $21.4 billion, or 42 percent of the year-to-date target. Overall, while China has excelled on the agricultural front, it remains considerably short on the energy purchases front—although, to be fair, China and the global economy have had to deal with economic consequences of COVID-19 which struck immediately after the signing of the Phase One agreement.

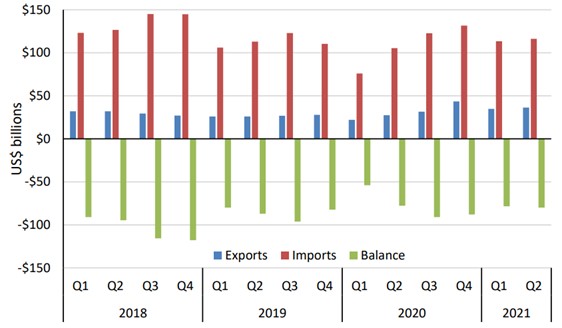

The overall state of the United States’ bilateral trade deficit with China, too, remains more-or-less unchanged. As the chart above shows, while the United States’ bilateral goods deficit has moderated somewhat from its 2018 highs, it still remains at an elevated level. The Phase One agreement’s market purchases chapter cannot be said to have accomplished its purpose successfully. And nor can the broader strategy of imposing unilateral Section 301 tariffs on Chinese imports—illegal, as they have subsequently been found to be at the WTO—be considered an overall success either.

Democratic administrations in the post-Cold War period have typically tended to shy away from carrying the political cross of regional and multilateral trade liberalization. With the exception of the second Barack Obama administration, which fought the difficult fight to obtain trade promotion authority (TPA) and steer the Trans-Pacific Partnership (TPP) negotiations to a successful conclusion, no other Democratic administration has initiated a major regional or multilateral trade negotiation over the past three decades. And even when Democratic administrations have shepherded the ratification of major regional or multilateral trade agreements through Congress, such as the Uruguay Round agreement or the North America Free Trade Agreement (NAFTA) during the first Clinton administration or the Korea-U.S. Free Trade Agreement (KORUS) during the first Obama administration, the agreements were more-or-less negotiated by their Republican predecessors and ratified on the strength of Republican votes. The Biden administration—staffed as it is at the senior policy levels by some who cut their teeth opposing the passage of free trade agreements through Congress—appears to be following in the vein of its Democratic predecessors.

USTR Tai’s less-than-compelling trade policy vision, as unexceptional as it might seem at first glance in context of prior Democratic administrations, nevertheless masks a more troubling dimension emerging within the body politic of American trade. The Democrats never did put up the votes to push preferential trade agreements across the finish line. With the Republican Party—hitherto a relative bastion of free trade thinking—now bending to ex-President Trump’s economic nationalist will, the fraying of the Beltway’s post-World War II consensus on trade liberalism appears increasingly apparent. Should the rank-and-file segments of the Republican party defect from its pro-trade moorings, this decades-old consensus could be shot through with harsh streaks of protectionism.

Past periods of economic upheaval have provided fertile breeding ground for Congress and the White House to come together and augment or reinterpret the statute books with tough trade enforcement tools. The risk, going forward, is that such tools are authorized or reinterpreted, perhaps from a labor standards standpoint in a Democratic administration, and thereafter employed in a manner that is inconsistent with the United States’ international trade commitments. In which case, the larger rules-bound multilateral trading system—not just U.S.-China economic ties—will also be worse off.

The Institute for China-America Studies is an independent nonprofit, nonpartisan research organization dedicated to strengthening the understanding of U.S.-China relations through expert analysis and practical policy solutions.

1919 M St. NW Suite 310,

Washington, DC 20036

icas@chinaus-icas.org

(202) 968-0595

© 2025 INSTITUTE FOR CHINA-AMERICA STUDIES. ALL RIGHTS RESERVED.